In the News:

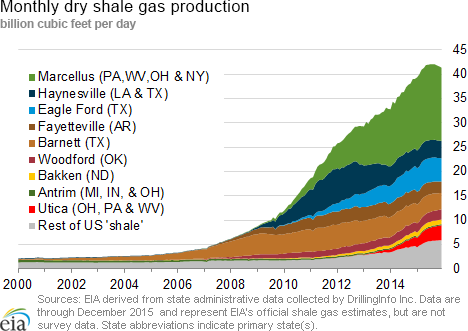

New Northeast pipelines help boost gas production 18%

In just the past six weeks, natural gas production in the Northeast has averaged 18% more than the year-ago period, according to Bentek Energy. The area includes the prolific Marcellus and Utica shales.

New infrastructure additions coming online in the past several months have likely contributed to year-over-year growth. But while Marcellus production has grown rapidly over the past several years, pipelines to move these increasing volumes out of the Northeast to consumption centers have not grown as quickly, largely because infrastructure projects have long lead times. Insufficient takeaway capacity will generally result in lower prices in the producing region and higher prices in the receiving region than would have been expected otherwise.

However, there were several important projects that came online in late 2015 or early 2016, totaling 4.2 billion cubic feet a day (Bcf/d) of flowing-gas capacity. They include:

- The reversal project for the Rockies Express Pipeline (REX), which began its first westbound flows in June 2014, brought additional capacity online in September 2015. With its recent expansion, REX can flow natural gas bidirectionally between Ohio and Indiana.

- In late 2015, Texas Eastern Transmission Company's (Tetco) OPEN project added 550 million cubic feet per day (MMcf/d) of westbound pipeline takeaway capacity out of Ohio.

- Columbia Gas Pipeline's East Side Expansion is a 310-MMcf/d project that flows natural gas produced in Pennsylvania to Mid-Atlantic markets.

- Tennessee Gas Pipeline's Broad Run Flexibility Project is a 590-MMcf/d project originating in West Virginia that moves natural gas to the Gulf Coast states.

- Tetco's Uniontown-to-Gas City project flows up to 425 MMcf/d of natural gas produced in the Marcellus region to Indiana.

- Williams Transcontinental Pipeline's Leidy Southeast project provides additional capacity to take Marcellus natural gas to Transco's mainline, which extends from Texas to New York. From there, the natural gas serves both Mid-Atlantic and Gulf Coast markets.

Overview:

(For the Week Ending Wednesday, February 10, 2016)

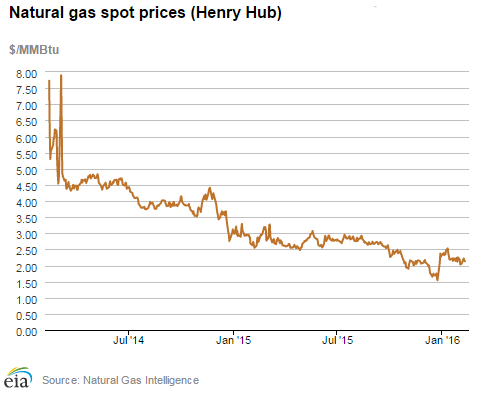

- Natural gas prices generally fell this report week (Wednesday, January 27, to Wednesday, February 3), with more dramatic declines in the northeastern United States. The Henry Hub spot price fell from $2.24 per million British thermal unit (MMBtu) last Wednesday to $2.06/MMBtu yesterday.

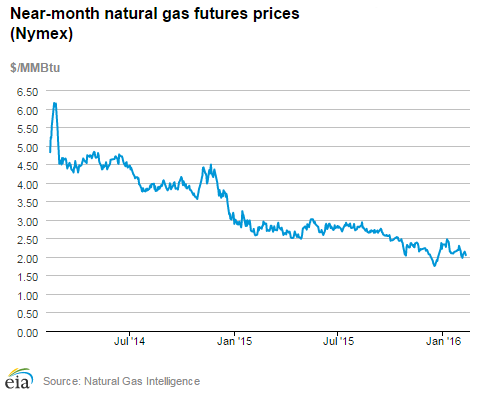

- At the New York Mercantile Exchange (Nymex), the price of the near-month (March 2016) contract fell from $2.189/MMBtu last Wednesday to $2.038/MMBtu yesterday.

- Working natural gas in storage decreased by 152 billion cubic feet (Bcf), declining to 2,934 Bcf as of Friday, January 29. The net withdrawal from storage resulted in storage levels 20% above a year ago and 18% above the five-year (2011–15) average for this week.

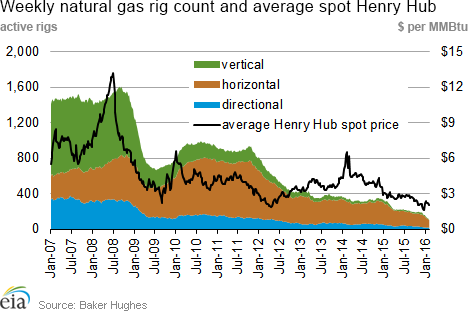

- The total oil and natural gas rig count declined by 18 units, with 619 units in service for the week ending Friday, January 29, according to data from Baker Hughes Incorporated. The oil rig count decreased by 12 units to 498, and the natural gas rig count fell by 6 units to 121. This is the fourth consecutive double-digit weekly decline and the lowest recorded natural gas rig count in the Baker Hughes dataset, which goes back to 1987.

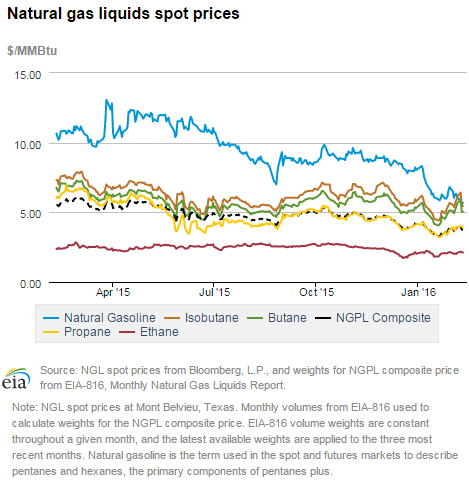

- The natural gas plant liquids (NGPL) composite price at Mont Belvieu, Texas, rose by 9.0% to $3.67/MMBtu for the week ending Friday, January 29. The spot prices of all liquids products increased this week, with ethane up 7.2%; propane, 9.5%; butane, 13.6%; isobutane, 14.2%; and natural gasoline, 4.7%. Despite this week's increase, prices are still relatively low.

Prices/Demand/Supply:

Natural gas prices decline. Temperatures were significantly warmer this report week across most of the country, and natural gas prices fell at most locations across the country. Natural gas markets appeared to reflect Punxsutawney Phil's prediction for an early spring, as temperatures were mild through much of the United States this week, and residential and commercial consumption declined. Likely in response to warmer weather and lower consumption, the Henry Hub spot price fell from $2.24/MMBtu last Wednesday to $2.06/MMBtu yesterday, February 3. At the Chicago Citygate, the spot price fell from $2.22/MMBtu last Wednesday to $2.07/MMBtu yesterday. Similarly, west of the Mississippi River, prices declined as well. In the Rocky Mountains, the spot price at the Opal Hub in Wyoming opened the report week at $2.07/MMBtu and ended yesterday at $2.01/MMBtu. At the PG&E Citygate in California, natural gas prices fell from $2.46/MMBtu last Wednesday to $2.27/MMBtu yesterday.

Northeast prices fall. Prices in the New York and Boston areas generally trade at a premium of several dollars per MMBtu above the Henry Hub spot price in times of high consumption, but tend to trade below this national benchmark in times of milder weather. This week, prices at both these market locations fell below the Henry Hub spot price as temperatures warmed up. At the Algonquin Citygate, which serves Boston, prices fell from $3.52/MMBtu last Wednesday to $1.90/MMBtu yesterday. Boston-area prices fell throughout the week. At Transcontinental Pipeline's Zone 6 trading point serving New York City, prices fell from $2.43/MMBtu last Wednesday to $1.79/MMBtu yesterday.

Marcellus prices decline. Week-over-week, spot prices at major Marcellus trading hubs declined. At Dominion South in northwest Pennsylvania, prices began at $1.60/MMBtu last Wednesday and ended the report week at $1.35/MMBtu yesterday. Similarly, on Transco's Leidy Line in northern Pennsylvania, prices fell from $1.38/MMBtu to $1.22/MMBtu Wednesday-to-Wednesday. At Tennessee Pipeline's Zone 4 Marcellus trading point, prices fell from $1.36/MMBtu to $1.19/MMBtu Wednesday-to-Wednesday.

Nymex prices fall. The price of the Nymex March 2016 contract fell from $2.189/MMBtu last Wednesday to $2.038/MMBtu yesterday. The price of the 12-month strip (the 12 contracts between March 2016 and February 2017) fell from $2.412/MMBtu last Wednesday to $2.384/MMBtu yesterday.

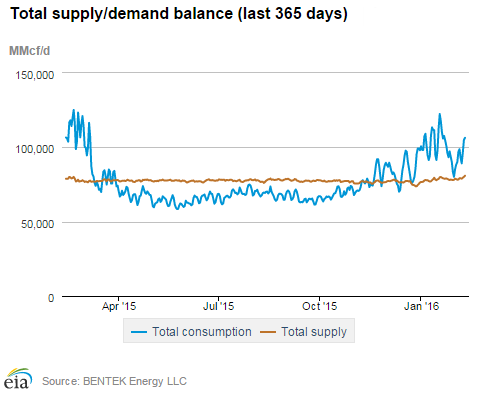

Production rises. Dry natural gas production rose 0.8% week over week and is 0.5% greater than the same week last year, according to Bentek data. Bentek also noted that production from the Northeast (which includes the Marcellus and Utica formations) has been at record levels in recent weeks. U.S. imports of natural gas from Canada fell 12.2%. Declines in imports in the West and Northeast offset a slight increase in imports to the Midwest. LNG sendout declined by 31.1%.

Heating consumption falls substantially. U.S. consumption fell by 14.3%, driven by a large decrease in residential/commercial consumption. According to Bentek data, residential/commercial consumption, which is largely used for heating, fell by 20.6%. Industrial consumption fell by 4.4%, and consumption of natural gas for electric power generation fell by 11.3%, both of which are also affected by changing temperatures, but to a lesser degree than residential and commercial customers. U.S. exports of natural gas to Mexico increased by 10.5%.

Storage

Withdrawals from storage are smaller than average but greater than last year. Net withdrawals from working gas totaled 152 Bcf, falling 8% below the the 5-year (2011–15) average net withdrawal of 165 Bcf. Still, the withdrawal was 40 Bcf larger last year's pull for the same storage week. This marks the fifth consecutive week of triple-digit storage withdrawals in the Lower 48 states. Working gas levels remain relatively high, with a surplus of 490 Bcf (20%) compared with last year at this time, and 445 Bcf (18%) higher than the 5-year average.

Withdrawals from working gas are within market expectations. Market analysts predicted working gas draws totaling 154 Bcf for the week, on average. Prices on the Nymex exhibited their customary increased levels of variability following the release of EIA's Weekly Natural Gas Storage Report at 10:30 a.m. However, trading occurred in an uncharacteristically narrow range, within a penny of $1.99/MMBtu. Trading also was fairly light, with 254 trades occurring at 10:30 a.m., and an average of 49 trades/second in the 30 seconds after the release. This compares to 815 trades in the same period last week, a relatively high volume

Temperatures are warmer than normal during the storage week. Temperatures for the storage report week averaged just less than 36°F, about 3°F above the normal level for this time of year and 2°F below the level reported last year at this time. The warming temperatures decreased heating degree days (HDD) by 12% from the previous week, with reported levels totaling 205 for the week. Cumulative HDD remain about 13% below normal thus far in the heating season, which began November 1.

See also:

")

| Spot Prices ($/MMBtu) | Thu, 04-Feb |

Fri, 05-Feb |

Mon, 08-Feb |

Tue, 09-Feb |

Wed, 10-Feb |

|---|---|---|---|---|---|

| Henry Hub |

2.05 |

2.08 |

2.22 |

2.17 |

2.13 |

| New York |

2.07 |

2.15 |

2.90 |

3.46 |

5.99 |

| Chicago |

2.06 |

2.09 |

2.27 |

2.23 |

2.17 |

| Cal. Comp. Avg,* |

2.09 |

2.06 |

2.16 |

2.09 |

2.03 |

| Futures ($/MMBtu) | |||||

| March contract |

1.972 |

2.063 |

2.140 |

2.098 |

2.046 |

| April contract |

2.062 |

2.137 |

2.189 |

2.149 |

2.111 |

| *Avg. of NGI's reported prices for: Malin, PG&E citygate, and Southern California Border Avg. | |||||

| Source: NGI's Daily Gas Price Index | |||||

| U.S. natural gas supply - Gas Week: (2/3/16 - 2/10/16) | ||

|---|---|---|

Percent change for week compared with: |

||

last year |

last week |

|

| Gross production | 1.18%

|

0.46%

|

| Dry production | 1.17%

|

0.46%

|

| Canadian imports | 8.15%

|

13.91%

|

| West (net) | 15.20%

|

1.51%

|

| Midwest (net) | 72.53%

|

13.13%

|

| Northeast (net) | -58.58%

|

206.34%

|

| LNG imports | -15.27%

|

10.91%

|

| Total supply | 1.56%

|

1.41%

|

| Source: BENTEK Energy LLC | ||

| U.S. consumption - Gas Week: (2/3/16 - 2/10/16) | ||

|---|---|---|

Percent change for week compared with: |

||

last year |

last week |

|

| U.S. consumption | 2.7%

|

12.8%

|

| Power | 21.6%

|

15.9%

|

| Industrial | 0.5%

|

3.5%

|

| Residential/commercial | -5.3%

|

16.2%

|

| Total demand | 3.7%

|

12.2%

|

| Source: BENTEK Energy LLC | ||

| Rigs | |||

|---|---|---|---|

Fri, February 05, 2016 |

Change from |

||

last week |

last year |

||

| Oil rigs | 467 |

-6.22% |

-59.04% |

| Natural gas rigs | 104 |

-14.05% |

-66.88% |

| Miscellaneous | 0 |

0.00% |

-100.00% |

| Rig numbers by type | |||

|---|---|---|---|

Fri, February 05, 2016 |

Change from |

||

last week |

last year |

||

| Vertical | 60 |

-18.92% |

-74.25% |

| Horizontal | 458 |

-5.95% |

-57.90% |

| Directional | 53 |

-8.62% |

-60.74% |

| Source: Baker Hughes Inc. | |||

| Working gas in underground storage | ||||

|---|---|---|---|---|

Stocks billion cubic feet (bcf) |

||||

| Region | 2016-02-05 |

2016-01-29 |

change |

|

| East | 620 |

641 |

-21 |

|

| Midwest | 739 |

767 |

-28 |

|

| Mountain | 151 |

159 |

-8 |

|

| Pacific | 258 |

271 |

-13 |

|

| South Central | 1,096 |

1,096 |

0 |

|

| Total | 2,864 |

2,934 |

-70 |

|

| Source: U.S. Energy Information Administration | ||||

| Working gas in underground storage | |||||

|---|---|---|---|---|---|

Historical comparisons |

|||||

Year ago (2/5/15) |

5-year average (2011-2015) |

||||

| Region | Stocks (Bcf) |

% change |

Stocks (Bcf) |

% change |

|

| East | 508 |

22.0 |

524 |

18.3 |

|

| West | 581 |

27.2 |

589 |

25.5 |

|

| Producing | 130 |

16.2 |

144 |

4.9 |

|

| Total | 2,291 |

25.0 |

2,321 |

23.4 |

|

| Source: U.S. Energy Information Administration | |||||

| Temperature -- heating & cooling degree days (week ending Feb 04) | ||||||||

|---|---|---|---|---|---|---|---|---|

HDD deviation from: |

CDD deviation from: |

|||||||

| Region | HDD Current |

normal |

last year |

CDD Current |

normal |

last year |

||

| New England | 170

|

-103

|

-166

|

0

|

0

|

0

|

||

| Middle Atlantic | 182

|

-80

|

-121

|

0

|

0

|

0

|

||

| E N Central | 201

|

-88

|

-95

|

0

|

0

|

0

|

||

| W N Central | 225

|

-76

|

-75

|

0

|

0

|

0

|

||

| South Atlantic | 116

|

-61

|

-73

|

10

|

3

|

6

|

||

| E S Central | 101

|

-78

|

-77

|

1

|

0

|

1

|

||

| W S Central | 78

|

-50

|

-43

|

6

|

2

|

6

|

||

| Mountain | 233

|

12

|

61

|

0

|

-1

|

0

|

||

| Pacific | 127

|

15

|

58

|

0

|

0

|

0

|

||

| United States | 163

|

-54

|

-54

|

3

|

1

|

2

|

||

|

Note: HDD = heating degree-day; CDD = cooling degree-day Source: National Oceanic and Atmospheric Administration | ||||||||

Average temperature (°F)

7-Day Mean ending Feb 04, 2016

Source: NOAA/National Weather Service

Deviation between average and normal (°F)

7-Day Mean ending Feb 04, 2016

Source: NOAA/National Weather Service